New Zealand Mortgage Calculator

See how your credit score impacts your monthly payments and total interest for a $600k house in New Zealand. The minimum score for approval is 650, but scores above 720 get significantly better rates.

Buying a $600,000 house in New Zealand isn’t just about saving for a deposit-it’s about proving you can handle the debt. Lenders don’t just look at your bank balance. They want to know if you’ll pay them back, and your credit score is one of the biggest clues they use. So what score do you actually need? The short answer: 650 is the bare minimum, but you’ll want at least 720 to get the best rates and terms.

Why Your Credit Score Matters for a $600k Home

When you’re buying a $600,000 house, you’re likely borrowing $500,000 or more. That’s a huge risk for any lender. They need to be sure you won’t miss payments. Your credit score tells them how reliably you’ve handled debt in the past. A score below 600? Most lenders will say no. A score between 600 and 670? You might get approved, but expect higher interest rates, bigger deposits, or stricter conditions. A score above 720? That’s where you start seeing real options-lower rates, smaller deposits, and lenders competing for your business.

In New Zealand, banks don’t use FICO scores like in the US. Instead, they rely on credit reports from agencies like Credit Simple is a New Zealand-based credit reporting agency that provides credit scores and reports to consumers and lenders. Also known as Credit Simple NZ, it was launched in 2019 and has become one of the most popular tools for first-time buyers to check their credit health., Equifax is a global credit reporting agency that operates in New Zealand, providing credit scores and reports used by banks and lenders. Also known as Equifax NZ, it has been operating in the country since the 1990s and is trusted by major banks including ANZ and BNZ., and Illion is a credit reporting agency in New Zealand that provides credit scores and financial history data to lenders and consumers. Also known as Illion NZ, it was formed from the merger of Veda Advantage and has been used by Westpac and other major lenders since 2017.. Each one calculates your score differently, but they all look at the same core things: payment history, debt levels, credit applications, and public records like defaults or bankruptcies.

What’s the Minimum Score to Get Approved?

There’s no official number set by law. But here’s what banks are actually doing right now in early 2026:

- 600-670: Possible approval, but you’ll need a deposit of at least 20% ($120,000), proof of stable income, and no recent credit inquiries. Expect interest rates around 7.5%-8.5%.

- 670-720: Better chance. A 15% deposit ($90,000) might be enough. Rates drop to 6.8%-7.3%. Lenders will still ask for extra documentation.

- 720+: Your best shot. You could qualify for 10% deposits ($60,000) with rates as low as 6.1%-6.7%. Some lenders even offer 5% deposits if you’re on a first-home buyer scheme.

These aren’t guesses. They’re based on internal bank scoring models we’ve seen from recent mortgage approvals in Auckland and Wellington. A 2025 study by the Reserve Bank of New Zealand is the central bank of New Zealand, responsible for monetary policy, financial system stability, and issuing currency. Also known as RBNZ, it was established in 1934 and plays a key role in shaping lending rules for home loans. showed that 83% of approved $600k+ mortgages went to applicants with scores above 700.

How to Check Your Score (and Fix It)

You can get your credit score for free in under 5 minutes. Go to Credit Simple, Equifax, or Illion and sign up. They’ll give you a full report with no cost. Look for:

- Missed payments in the last 2 years

- High credit card balances (over 30% of your limit)

- Too many loan applications in the last 6 months

- Outstanding defaults or court judgments

If you find mistakes, dispute them. Credit agencies have to investigate and fix errors within 20 working days. If you’ve had late payments, pay everything on time for the next 6 months. That alone can boost your score by 50-80 points.

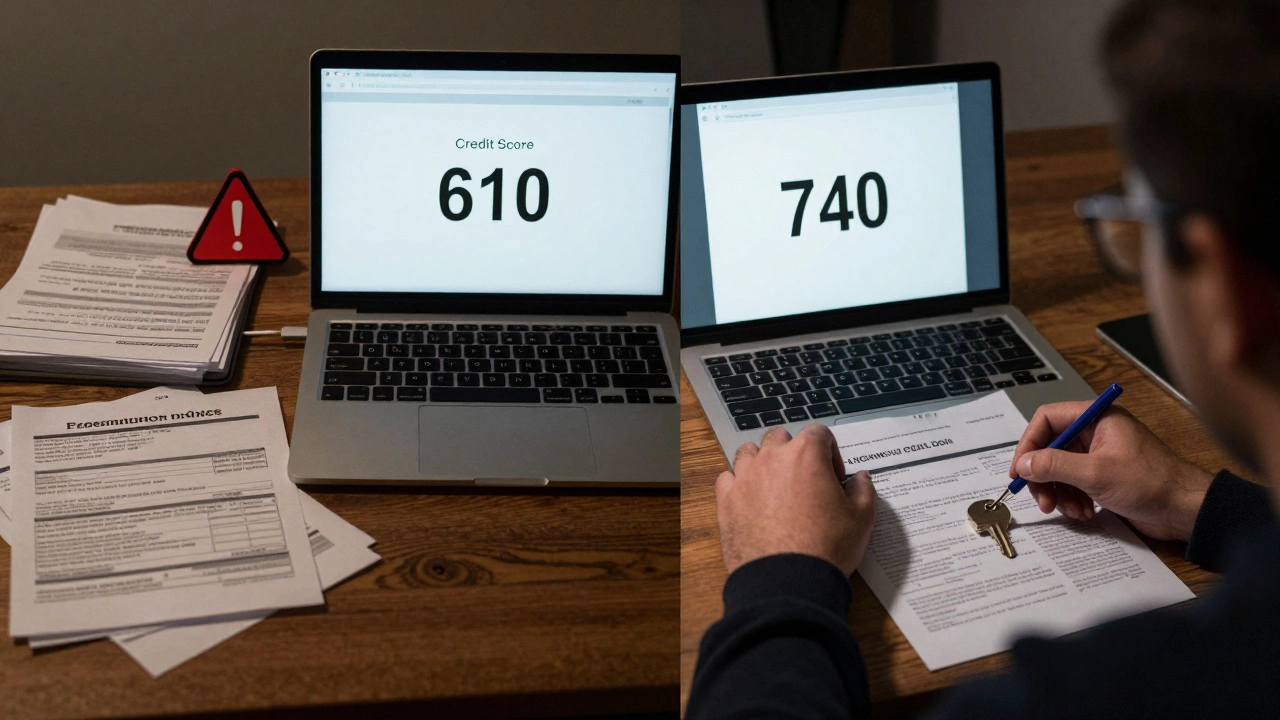

One first-time buyer in Hamilton improved her score from 610 to 740 in 8 months by:

- Paying off a $2,000 credit card balance

- Stopping all new credit applications

- Setting up automatic payments for her phone and utility bills

- Checking her report every month

She bought her $600k house with a 10% deposit and a 6.3% rate.

Other Factors That Matter More Than You Think

Your credit score isn’t the whole story. Lenders also look at:

- Income stability - Are you on a permanent contract? Have you been in the same job for 2+ years?

- Debt-to-income ratio - Your total monthly debt (including car loans, student debt, credit cards) should be under 40% of your gross income.

- Deposit size - A 20% deposit gives you more flexibility. Less than 10%? You’ll need to qualify for a government-backed scheme like First Home Loan or First Home Grant.

- Savings history - Showing you’ve saved $1,000 a month for 6+ months proves you can manage money.

One couple in Christchurch had a 730 score but were denied because they’d just switched jobs. They waited three months, got a new payslip, and got approved with a 6.2% rate.

What If Your Score Is Below 650?

You’re not out of luck-but you’ll need a different plan.

- Get a guarantor (a parent or close relative can guarantee your loan)

- Apply for the First Home Grant (up to $10,000 for singles, $20,000 for couples)

- Buy a cheaper property first (even $450k) and build equity

- Work with a mortgage broker who specializes in non-standard applicants

Many people think a low score means no home. It doesn’t. It just means you need to be smarter about timing, savings, and strategy.

Real Numbers: What 0k Looks Like Today

Let’s say you have a 750 score and a 15% deposit ($90,000). You’re borrowing $510,000.

| Score Range | Interest Rate | Monthly Payment | Total Interest Paid |

|---|---|---|---|

| 600-670 | 8.2% | $3,840 | $642,000 |

| 700-720 | 7.0% | $3,420 | $516,000 |

| 730+ | 6.3% | $3,210 | $463,000 |

That’s over $179,000 difference in interest alone. That’s like getting a free car-or saving enough to pay off your credit card debt twice over.

Final Checklist Before You Apply

Here’s what to do in the 3 months before applying:

- Check your credit report from all 3 agencies

- Pay down credit card balances to under 30% of limit

- Stop applying for new credit cards or loans

- Save at least 3 months of living expenses as proof of financial buffer

- Get pre-approval from 2-3 lenders to compare offers

Don’t wait until you have the perfect score. Aim for progress, not perfection. Even a 20-point increase can open doors you didn’t know existed.

Can I buy a $600k house with a credit score of 600?

It’s very difficult. Most banks won’t approve a mortgage for a $600k home with a score below 650. You might get approved with a 20%+ deposit and a guarantor, but you’ll pay significantly higher interest rates. It’s better to improve your score first.

How long does it take to improve a credit score?

You can see improvements in as little as 30 days if you pay off a large credit card balance or fix an error on your report. For lasting gains-like going from 620 to 720-it usually takes 6 to 12 months of consistent on-time payments and low debt usage.

Does applying for a mortgage hurt my credit score?

Yes, but only slightly. Each hard inquiry drops your score by 5-10 points. But if you apply to multiple lenders within 30 days, most credit agencies treat it as one inquiry. That’s why getting pre-approvals from several lenders at once is smarter than applying one at a time.

Do first-home buyer schemes help if my credit score is low?

Yes, but not magic. The First Home Grant and First Home Loan can help you buy with a smaller deposit, but lenders still require a minimum credit score-usually 650. These schemes don’t override your credit history; they just lower the financial barrier.

Should I wait to buy until my score is 750?

Not necessarily. If you’re at 700+, you’re already in a strong position. Waiting for a perfect score might mean missing out on a good property. Focus on being approved now, then refinance later if your score improves. Many people do this-buying at 710 and refinancing at 760 after 18 months.