Mortgage Affordability Calculator for NZ

Calculate how much home you can afford with a $70,000 salary in New Zealand based on lender requirements. This tool uses NZ banking standards including the 40% debt-to-income ratio, standard living expenses, and interest rate buffers.

Maximum Mortgage Amount:

$0

Maximum Home Price:

$0

Monthly Mortgage Payment:

$0

Debt-to-Income Ratio:

0%

Key Insights for Your Situation

Your results will appear here after calculation.

With a $70,000 salary, you might think buying a home in New Zealand is out of reach-especially if you’re looking in Auckland, Hamilton, or Wellington. But it’s not impossible. Many first-time buyers with similar incomes are securing homes every month. The real question isn’t just how much you can borrow-it’s what kind of home you can actually afford after taxes, living costs, and lender rules.

How lenders calculate your borrowing power

- Income: Lenders look at your gross annual income. For a $70,000 salary, they’ll use that number directly.

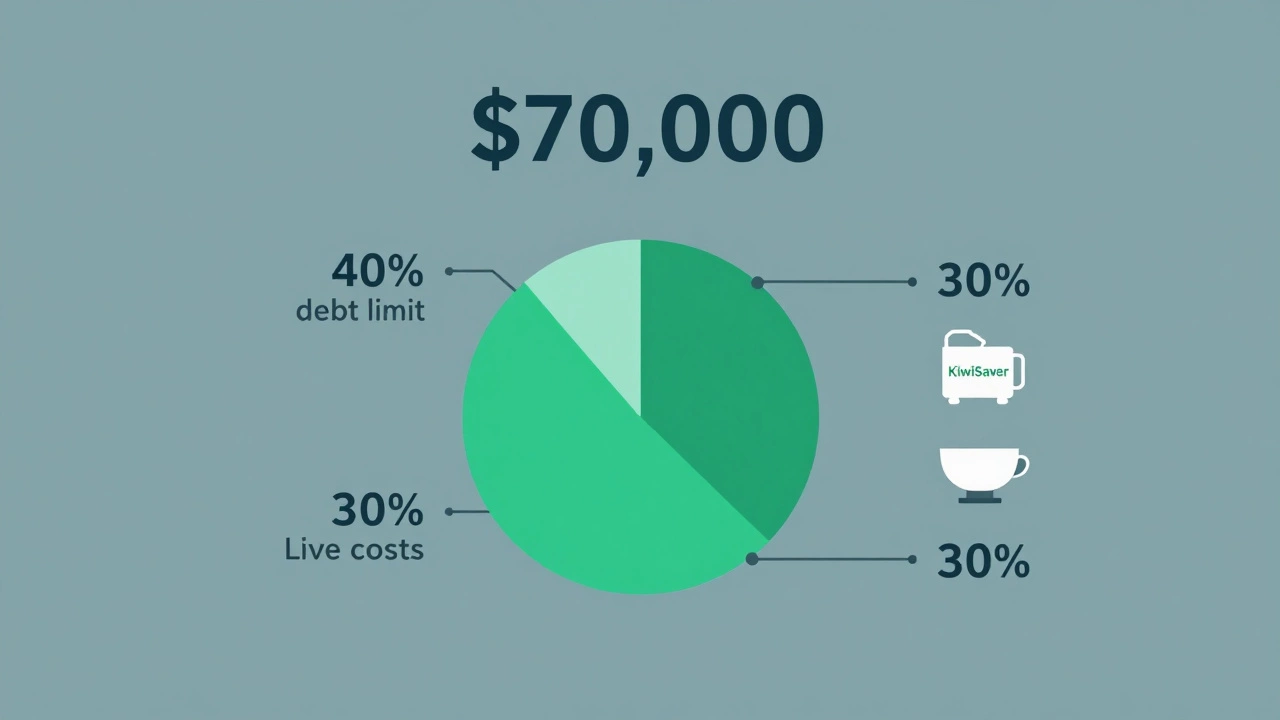

- Debt-to-income ratio: Most NZ banks cap your total monthly debt payments (including mortgage, car loans, credit cards) at 40% of your gross income. That means your total debt payments can’t exceed $2,333 per month.

- Living expenses: Banks use a standard living expense calculator (like the one from the Reserve Bank). For a single person, they assume you spend $1,200-$1,500 per month on food, transport, bills, and other basics. For a couple, it’s $1,800-$2,200.

- Interest rate buffer: Lenders test your loan at a rate 2-3% higher than the current rate to make sure you can still pay if rates go up. Right now, they’re using around 7.5%-8% for assessment, even if you’re getting a 6.5% deal.

Let’s say you’re single, no other debts, and you’re applying for a mortgage in early 2026. You’ve got $70,000 gross income. After tax, you take home about $5,400 per month. Lenders will subtract your estimated living costs ($1,300) and any other debt payments (say, $0). That leaves you with $4,100 to cover your mortgage. But they’ll test you at 8% interest. At that rate, you’d qualify for a loan of around $480,000-$510,000.

What deposit do you need?

You can’t just borrow 100% of the home’s price. Most lenders require at least a 10% deposit for first-time buyers. That means if you want to buy a $500,000 house, you need $50,000 saved up. If you’re buying a $400,000 home, you need $40,000.

Here’s the catch: the average house in Auckland is around $950,000. That’s way beyond what a $70,000 salary can support-even with a 20% deposit. But you don’t have to buy there. In places like Tauranga, Hamilton, or even outer suburbs of Auckland like Papakura or Manukau, you can find 3-bedroom homes between $600,000 and $750,000. With a 15% deposit, you’d need $90,000-$112,000 saved. That’s tough, but doable with KiwiSaver and family help.

KiwiSaver and government help

If you’ve been contributing to KiwiSaver for at least three years, you can withdraw your own contributions, employer contributions, and government kick-start to use as a deposit. Most first-time buyers pull out $20,000-$35,000 this way.

There’s also the First Home Loan scheme (run by Kāinga Ora). It lets you buy with as little as a 5% deposit if your income is under $95,000 (single) or $140,000 (couple). For a $70,000 earner, you’re eligible. The maximum property price varies by region-in Auckland, it’s $850,000. In other areas, it’s higher. You’ll still need to pass the affordability test, but the lower deposit requirement makes a big difference.

Real examples from 2026

Meet Sarah, 28, from Tauranga. She earns $72,000 a year, has $38,000 in KiwiSaver, and no debt. She found a 3-bedroom townhouse for $580,000. With her savings, she put down a 12% deposit ($69,600). She got a 6.8% fixed rate for 3 years. Her monthly mortgage payment? $3,120. She’s still under the 40% debt-to-income limit. Her living costs are $1,100. She has $1,200 left over each month after mortgage and essentials. She’s not rich-but she owns a home.

Compare that to Jake, 31, in Auckland. He earns $70,000, has $25,000 saved, and a $5,000 car loan. His debt-to-income ratio is already at 35% before even considering a mortgage. He can only afford a $420,000 home with a 10% deposit. That means he’s looking at a small 2-bedroom unit in Papatoetoe or a fixer-upper in Manurewa. He’s waiting for interest rates to drop further before applying.

What you can realistically afford

With a $70,000 salary in 2026, here’s what’s possible:

- Maximum loan: $480,000-$520,000 (depending on deposit and living costs)

- Maximum home price: $530,000-$580,000 (with 10-15% deposit)

- Best regions: Hamilton, Tauranga, Napier, Lower Hutt, Porirua, Manukau

- Minimum deposit: $50,000-$85,000 (with KiwiSaver help, you can cut that in half)

- Monthly mortgage payment: $2,900-$3,400 (at 6.5%-7.5% interest)

You won’t get a beachfront apartment in Mission Bay. But you can get a solid, safe, modern home in a good neighborhood with good schools, public transport, and room to grow.

How to increase your chances

- Save more than the minimum: Even $5,000 extra in your deposit can unlock better rates and higher borrowing power.

- Pay off small debts: A $3,000 credit card balance might seem small, but it can knock $50,000 off your borrowing limit.

- Use a mortgage broker: They know which lenders are flexible with first-time buyers. Some banks give extra weight to KiwiSaver contributions.

- Check your credit score: A score above 700 gets you better rates. Free tools like Credit Simple and Credit Simple NZ show you where you stand.

- Consider a joint application: If your partner earns $50,000, your combined income of $120,000 opens up much bigger options.

What to avoid

- Buying too close to your limit: If your mortgage eats up 80% of your take-home pay, you won’t survive a job loss or unexpected bill.

- Ignoring ongoing costs: Rates, insurance, rates, maintenance, and heating add $200-$400/month. Don’t forget them.

- Chasing the biggest house: A smaller, well-located home with room to add value is smarter than a large one that drains you.

- Waiting for prices to drop: In NZ, prices don’t crash-they stagnate. Interest rates drop faster than house prices. Lock in when rates are low, even if you have to compromise on size.

Next steps

Start by using the KiwiHomeFinder affordability calculator. Plug in your salary, savings, and location. Then, book a free 30-minute session with a licensed mortgage advisor. They’ll run your numbers, show you exactly what you qualify for, and help you avoid costly mistakes.

You don’t need to be rich to own a home. You just need to be prepared.

Can I get a mortgage with $70,000 salary if I have student debt?

Yes, but your student loan reduces your borrowing power. Lenders treat student debt differently than credit card debt. In New Zealand, student loans are interest-free while you’re living here, so they don’t count as high-risk debt. But they still appear on your credit file. A $20,000 student loan might reduce your mortgage limit by $15,000-$30,000, depending on your other expenses. Paying it down before applying can help.

How much deposit do I need if I’m using KiwiSaver?

You need at least 5% of the home price as a deposit from your own savings (not KiwiSaver). KiwiSaver funds can cover the rest of the deposit. For example, if you’re buying a $500,000 home, you need $25,000 from your own savings. You can then use $50,000 from KiwiSaver to make up the 15% total deposit. If you have $60,000 in KiwiSaver, you’re in a strong position.

Can I buy a house if I’m self-employed with $70,000 income?

It’s harder, but possible. Lenders want two years of tax returns to verify your income. If your income is steady and your business is stable, you can still qualify. Some lenders specialize in self-employed borrowers. You’ll likely need a larger deposit-15-20%-and a cleaner credit history. Getting a mortgage broker who understands small business income is critical.

Is $70,000 enough to buy in Auckland?

It’s tight, but not impossible. The average house in Auckland is $950,000, so you’d need a $190,000 deposit-unrealistic without family help. But in suburbs like Papakura, Manukau, or Henderson, you can find 3-bedroom homes between $700,000-$780,000. With a 15% deposit ($105,000-$117,000), KiwiSaver, and a joint application, it’s doable. You’ll need to be disciplined with savings and realistic about location.

What happens if interest rates go up after I buy?

Lenders already test you at rates 2-3% higher than what you’re offered. So if you’re approved for a 6.5% mortgage, they checked if you can afford 8.5%. That means you’re already prepared for most rate hikes. If rates jump beyond that, your monthly payment will increase-but you won’t be caught off guard. Fixing your rate for 2-3 years gives you stability. Many first-time buyers lock in for longer terms to avoid surprises.