Shared Ownership Income Calculator

Compare Your Income Options

See the real tax difference between taking money as an owner's draw or salary for your shared ownership home arrangement.

Your Annual Income

How This Applies to You

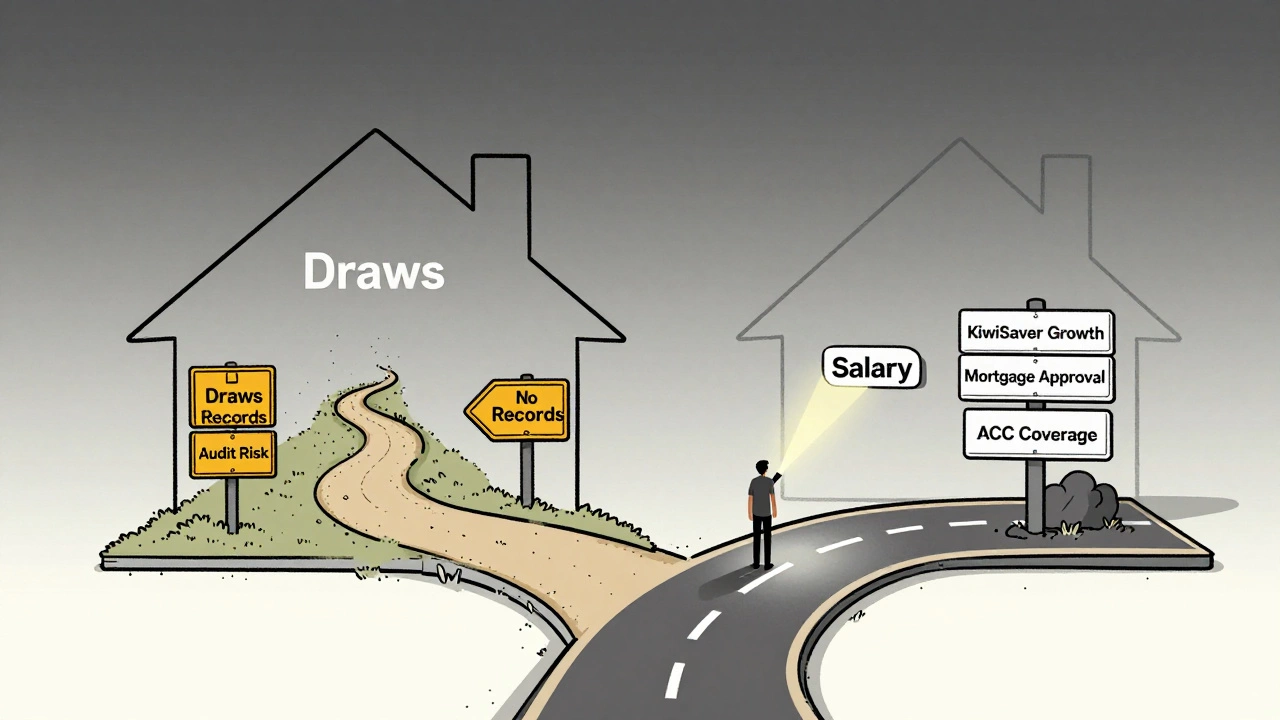

Key Considerations

• Income proof: Salary creates a clear paper trail for lenders

• Future planning: Salary builds KiwiSaver and ACC benefits

• Legal protection: Formal salary structure reduces audit risk

Who Should Choose Salary?

Owner's Draw

Salary

Key Differences

Draw: Simple but creates tax risks. No automatic KiwiSaver or ACC benefits.

Salary: Costs more upfront but builds long-term security and documentation.

When you co-own a home through a shared ownership scheme, you’re not just buying a place to live-you’re also running a small business. That’s the part most people overlook. If you’re part of a shared ownership arrangement where you live in the property and also rent out part of it-or if you’re using it as a base for a home-based business-you’ll eventually face a key question: Should you take money out as an owner’s draw or a salary? This isn’t just about cash flow. It’s about taxes, legal protection, and long-term financial health.

What’s the difference between owner’s draw and salary?

In a shared ownership setup, especially if you’ve structured it as a limited liability company (LLC) or partnership, the way you pay yourself matters more than you think.

An owner’s draw is money you take from your business’s profits. It’s not a wage. You don’t pay payroll taxes on it. You don’t get a payslip. You just withdraw what you need, whenever you need it. It’s flexible. But it’s also unstructured.

A salary, on the other hand, is a fixed, regular payment treated like an employee’s wage. It’s subject to income tax, ACC levies, and KiwiSaver deductions. It shows up on your IRD records, and your business has to file payroll reports. It’s predictable. But it’s also costly.

Here’s the catch: if you’re operating as a sole trader or informal partnership, the IRS-style rules don’t apply. But in New Zealand, the Inland Revenue Department still expects you to account for income fairly-even if you don’t call it a salary.

Why this matters in shared ownership

Shared ownership often means you’re splitting costs and income with someone else. Maybe you bought a four-bedroom house with a friend, lived in two rooms, and rented out the other two. Or maybe you’re part of a housing cooperative where you contribute labor and get reduced rent.

Either way, you’re generating income. And if that income isn’t reported properly, you risk:

- Underpaying your taxes

- Missing out on KiwiSaver contributions

- Having trouble proving income for mortgages or loans

- Creating disputes with your co-owner over who “earned” what

Let’s say you and your co-owner each get $1,200 a month from rent. You both live in the property. You don’t pay rent to each other. But you’re still earning income.

If you just take draws, IRD might see this as unreported business income. If you pay yourselves salaries, you’re building a paper trail. That matters when you apply for a mortgage later-or if IRD audits you.

Tax implications: draw vs salary

In New Zealand, there’s no payroll tax for sole traders. But there is income tax. And IRD doesn’t care what you call it-they care about what you earn.

Here’s the reality:

- Owner’s draw: You pay income tax on your share of the business profit at your personal tax rate (10.5%, 17.5%, 30%, or 33%). No ACC or KiwiSaver automatically deducted. You’re responsible for paying IRD instalments on time.

- Salary: You pay PAYE income tax, ACC levies (if you’re not exempt), and KiwiSaver (if you’re enrolled). Your business pays employer contributions to KiwiSaver (3%) and ACC levies (based on income). That adds up.

For example: if you earn $48,000 a year from rental income:

- As a draw: You pay about $9,600 in income tax (assuming 20% effective rate). No ACC. No KiwiSaver unless you voluntarily contribute.

- As a salary: You pay $7,920 in PAYE, $1,152 in ACC, and $1,440 in KiwiSaver (employee + employer). Total: $10,512.

So salary costs more upfront. But it gives you:

- Automatic KiwiSaver growth

- ACC coverage

- A clear income record

- Eligibility for student loans, child support calculations, or housing grants

What most shared ownership groups actually do

Most people in shared ownership arrangements don’t formalize this at all. They just split rent evenly and call it a day. But that’s risky.

A 2024 survey by the New Zealand Property Owners Association found that 68% of shared ownership households didn’t document income distribution. Of those, 41% later had trouble proving income when applying for a mortgage. Another 22% received unexpected tax bills because IRD reassessed their income as business earnings.

One Auckland couple, Mark and Lisa, bought a house in Mt Roskill under shared ownership. They rented out two rooms and lived in the rest. For three years, they took draws. No paperwork. Then Mark applied for a home loan to buy a second property. The bank asked for two years of tax returns. They had none. They had to restructure everything-paying back taxes, setting up a company, and starting salaries from scratch. It cost them $8,000 in fees and delays.

When to choose a draw

Owner’s draw makes sense if:

- You’re a sole trader or informal partner with low, irregular income

- You’re not planning to apply for loans or government support

- You’re comfortable managing your own tax payments

- You don’t need ACC or KiwiSaver benefits from this income

It’s simple. It’s flexible. But it’s also a ticking time bomb if your situation changes.

When to choose a salary

Paying yourself a salary is smarter if:

- You’re planning to buy more property

- You want to build KiwiSaver savings

- You’re in a formal partnership or LLC

- You’re applying for student loans, child support, or housing grants

- You want to prove income to banks or lenders

Even if it costs more now, it saves you headaches later. Plus, KiwiSaver contributions compound. If you start at 25 and contribute $100 a month, you’ll have over $70,000 by 65-even with modest returns.

What to do right now

If you’re in a shared ownership arrangement:

- Check how your arrangement is legally structured. Are you partners? Sole traders? Company owners?

- Track every dollar of rental income and expense. Use a free app like Xero or Wave.

- Calculate your annual profit. Divide it fairly between owners.

- Decide: Are you going to take draws, or set up regular salaries?

- If you choose salary: Register as an employer with IRD. Set up payroll. Start deductions.

- Keep records. Always. Even if you think it’s “just family.”

Don’t wait for IRD to come knocking. If you’re sharing ownership, you’re sharing responsibility. And that includes how you pay yourself.

Common mistakes to avoid

- Using personal bank accounts for business income. Mixing money makes audits harder.

- Assuming “no rent” means “no income.” IRD considers living rent-free as income if you’re renting out part of the property.

- Thinking “it’s just a friend.” Without a written agreement, disputes over money can end friendships.

- Ignoring KiwiSaver. You’re leaving thousands on the table if you don’t contribute.

Final thought

There’s no magic answer. But there is a smarter path.

Owner’s draw feels easier. But salary builds security. In shared ownership, where trust is everything, the most reliable thing you can do is create clear, documented systems. Not because you don’t trust your co-owner. But because the system protects you both-even if things change.

Start small. Track your income. Talk to an accountant. Set up one payroll run this month. That’s all it takes to start building a foundation that lasts.