Buying your first home in New Zealand feels exciting - until you hit the number that makes your stomach drop: the downpayment. If you're looking at a $200,000 house, you might think you need $40,000 upfront. But that’s not the whole story. In New Zealand, the actual amount you need to save can be much lower - and sometimes higher - depending on your situation. Let’s cut through the noise and show you exactly what you’re up against.

What counts as a downpayment?

A downpayment - or deposit - is the money you pay upfront when buying a home. The rest is covered by your mortgage. In New Zealand, lenders don’t just look at the house price. They look at your income, your credit history, your existing debts, and even how long you’ve been employed. That means two people buying the same $200,000 house might need totally different deposits.

Most lenders require at least 10% for first-time buyers. That’s $20,000 on a $200,000 home. But if you’re using KiwiSaver (and most first-timers do), you can get away with as little as 5% - which is just $10,000. That’s not a myth. It’s a real option under the First Home Loan scheme, run by Kāinga Ora.

Can you really buy with 5% down?

Yes - but only if you meet strict rules.

- You must be a first-time buyer (never owned property in New Zealand or overseas).

- Your household income must be under $120,000 (or $150,000 in Auckland, Wellington, and Christchurch).

- You need to have been contributing to KiwiSaver for at least three years.

- The house must be priced at or below the regional price cap - for most areas, that’s $550,000, but in Auckland it’s $750,000. A $200,000 house easily fits.

If you hit all these boxes, you can use your KiwiSaver savings as part of your deposit. Plus, you can get a government-backed loan for up to 20% of the home’s value. That means you only need to save 5% yourself. For a $200,000 house, that’s $10,000.

But here’s the catch: even if you’re eligible, lenders still want to see you can afford the monthly repayments. If you’re earning $60,000 a year and have $15,000 in credit card debt, you might still be turned down. Your debt-to-income ratio matters just as much as your deposit.

What if you can’t use KiwiSaver?

Not everyone qualifies. Maybe you’ve only been in KiwiSaver for two years. Maybe you’ve got a bad credit score. Maybe you’re self-employed and can’t prove your income. In those cases, most lenders will ask for 20% - $40,000 on a $200,000 home.

Why 20%? Because it’s the magic number that avoids Lenders’ Mortgage Insurance (LMI). LMI protects the lender if you default. If you put down less than 20%, you pay LMI - and that cost gets added to your loan. For a $200,000 house with a 10% deposit, LMI could add $5,000-$8,000 to your debt. That’s not a deposit - it’s a hidden cost.

So if you’re thinking about a 10% deposit without KiwiSaver, you’re not just saving $20,000. You’re saving $25,000-$28,000. That’s a big difference.

Other costs you can’t ignore

Even if you nail your deposit, there are other fees that eat into your savings.

- Legal fees: $1,500-$3,000 for your lawyer or conveyancer.

- Valuation fee: $300-$600. The bank needs to check the house is worth what you’re paying.

- Building inspection: $400-$800. Don’t skip this. A $200,000 house could have $30,000 worth of hidden damage.

- Moving costs: $500-$2,000 depending on distance and size.

- Home insurance: You’ll need it before settlement. Expect $800-$1,500 a year.

So if you’ve saved $10,000 for your deposit, you’ll need another $3,000-$7,000 for everything else. That’s why many first-timers aim for $15,000-$20,000 total savings before they start looking.

How long does it take to save?

Let’s say you’re earning $65,000 a year after tax. That’s about $5,400 a month. If you spend $3,500 on rent, bills, food, and transport, you’ve got $1,900 left. If you save $1,000 a month, you’ll hit $10,000 in 10 months. $20,000 in 20 months. $40,000? That’s 40 months - over three years.

But here’s the real trick: your location matters. In Whangarei or Napier, a $200,000 house might be a decent 3-bedroom. In Auckland, it’s a small unit in a rundown block. You might be better off looking at a $150,000 house in a quieter suburb. That cuts your deposit in half.

Don’t fixate on $200,000. Fixate on what you can afford long-term. A $180,000 house with a $9,000 deposit might be smarter than a $200,000 house with a $20,000 deposit - especially if the smaller house has lower rates, lower insurance, and lower rates.

What if you’re still stuck?

You’re not alone. Many first-timers are stuck between high prices and low savings. Here are three real options that work right now:

- Buy with a co-buyer. A family member, partner, or friend can be on the mortgage with you. Their income helps you qualify. Their savings help you reach your deposit. Just make sure you have a legal agreement.

- Use the First Home Grant. If you’re buying a new home or building one, you might qualify for up to $10,000 from the government. It’s separate from KiwiSaver and doesn’t need to be repaid.

- Look at state-owned homes. Kāinga Ora sells homes at below-market prices to first-time buyers. Some are as low as $160,000. They’re not glamorous, but they’re solid, and they come with a 5% deposit option.

Don’t wait for the perfect house. Wait for the right opportunity. A $200,000 house isn’t the goal - a home you can afford, maintain, and live in for ten years is.

What’s the bottom line?

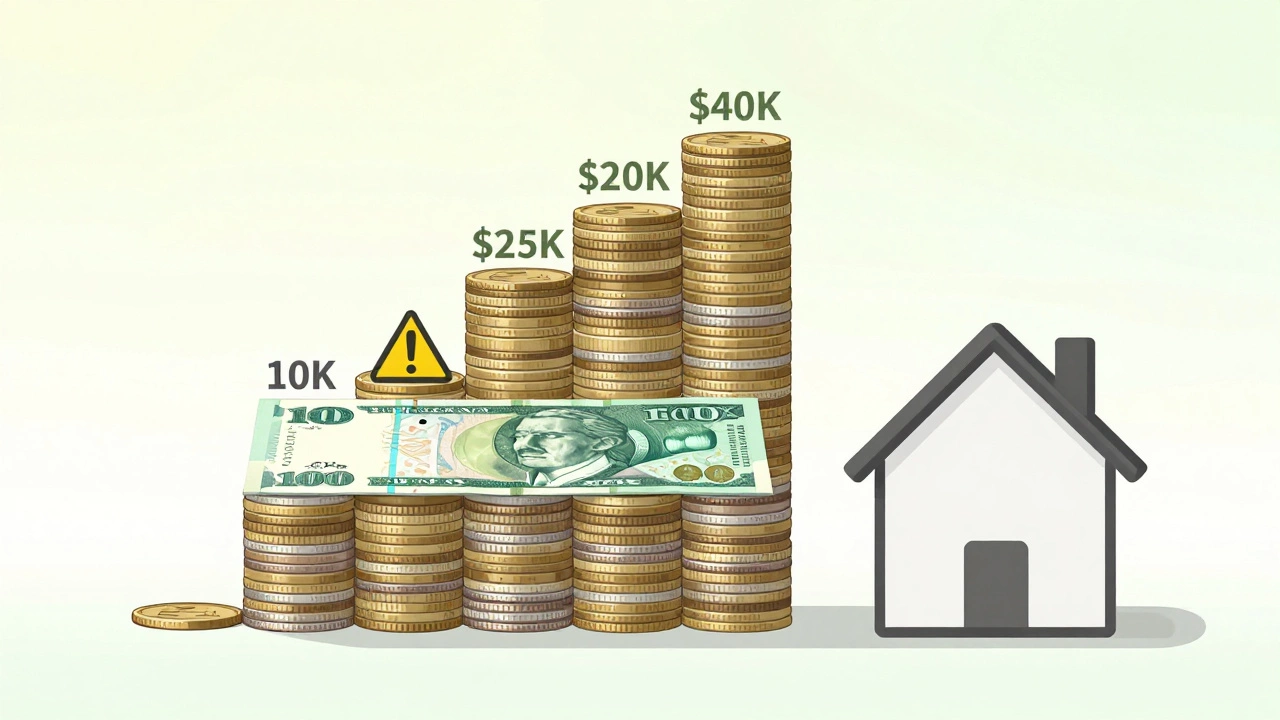

For a $200,000 house in New Zealand:

- Minimum deposit (with KiwiSaver): $10,000

- Typical deposit (no KiwiSaver): $20,000

- Recommended buffer (for fees): $25,000-$30,000

- Safe deposit (to avoid LMI): $40,000

Your path depends on your income, your savings, and your location. But here’s the truth: you don’t need to save $40,000 to buy your first home. You just need to know your options - and take the first step.