Business Valuation Calculator

Business Inputs

Valuation Results

When you hear the term business valuation is the process of estimating the economic worth of a company or its assets, the first thing that comes to mind is often a simple sales number. But a $1million top line tells only part of the story. In this guide we break down exactly how to turn that figure into a realistic valuation, step by step, using methods that work for small firms, start‑ups, and even shared‑ownership home ventures.

Why Sales Alone Can’t Tell the Whole Truth

Sales measure how much money comes in, not how much profit stays after expenses. A business with $1million in revenue could be barely breaking even, or it could be generating a healthy 30% net profit margin. That difference dramatically changes the price a buyer would pay. Moreover, the industry, growth trajectory, and asset structure (like property owned under a shared‑ownership scheme) all shape the final figure.

Key Valuation Concepts You Need to Know

- Revenue multiple is a ratio that applies a factor to annual sales to estimate value.

- EBITDA multiple is a multiple applied to earnings before interest, taxes, depreciation, and amortisation.

- Discounted cash flow (DCF) is a method that projects future cash flows and discounts them back to present value.

- Net profit is the bottom‑line earnings after all costs and taxes.

- Comparable company analysis is a technique that looks at recent sales of similar businesses.

1. Revenue Multiple - The Quick‑And‑Dirty Approach

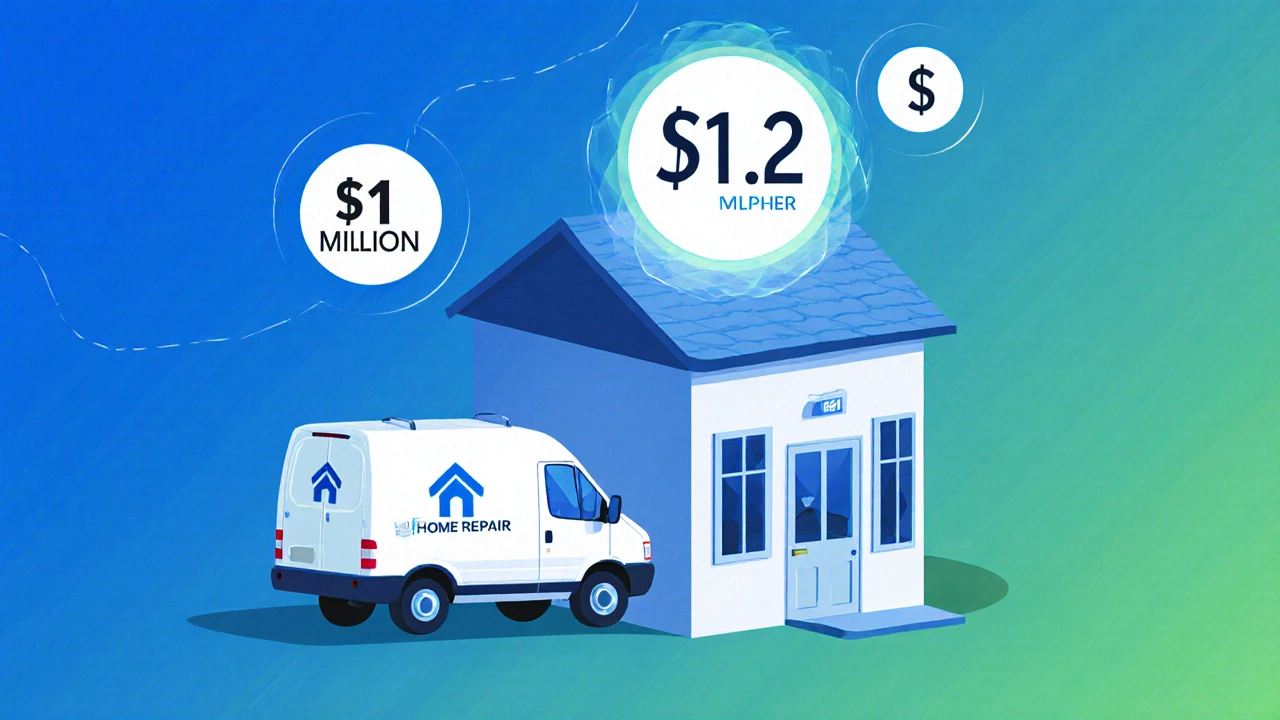

For many small businesses, especially service‑based ones, buyers start with a revenue multiple. The typical range is 0.5× to 2.5× annual sales, depending on industry risk and growth prospects. Let’s run a quick example:

- Annual sales: $1,000,000.

- Industry‑average multiple: 1.2× (e.g., local home‑services firms).

- Estimated value: $1,000,000 × 1.2 = $1.2million.

If your business runs in a high‑growth niche, you could push the multiple toward the top of the range. Conversely, if margins are thin, you’d stay near the bottom.

2. EBITDA Multiple - Focusing on Operating Profit

EBITDA strips out financing and accounting quirks, giving a cleaner picture of cash‑generating ability. The steps:

- Calculate EBITDA: Revenue - Cost of Goods Sold - Operating Expenses (add back depreciation & amortisation).

- Assume an EBITDA of $150,000 (15% margin, common for small retail).

- Apply an industry multiple, often 4× to 8× for low‑risk businesses.

- Value = $150,000 × 6 (mid‑range) = $900,000.

Notice how the EBITDA method can give a lower figure than pure revenue multiples because it accounts for profitability.

3. Discounted Cash Flow - The Deep Dive

DCF is favoured by investors who want a forward‑looking estimate. It requires projected cash flows for the next 5‑7 years and a discount rate reflecting risk (often the Weighted Average Cost of Capital, WACC).

- Project annual free cash flow: start with $150,000 EBITDA, subtract taxes and reinvestment, assume modest growth of 5% per year.

- Year‑1 cash flow: $150,000 × 1.05 = $157,500.

- Continue for 5 years, then calculate a terminal value using a 2% perpetual growth rate.

- Discount each year’s cash flow back at, say, 10% (typical small‑business WACC).

- Sum the discounted values - you’ll end up around $820,000 to $1million, depending on assumptions.

DCF is more work, but it captures growth potential and capital needs, which are crucial if the business owns property under a shared‑ownership model.

4. Adjusting for Shared‑Ownership Home Assets

If your $1million‑sales business also holds real‑estate - for example, a property‑management firm that operates shared‑ownership homes in Auckland is New Zealand’s largest city with a high demand for shared‑ownership housing - you must add the net asset value (NAV) of those properties.

Calculate NAV by taking the market value of each home (e.g., $300,000 each) and subtracting any mortgage balance. Add that total to the valuation derived from the income‑based methods. This can boost the overall worth by a few hundred thousand dollars, depending on the portfolio size.

5. Putting It All Together - A Practical Checklist

- Gather accurate financial statements for the past 3‑5 years.

- Determine profit margins and calculate EBITDA.

- Research industry multiples for revenue and EBITDA.

- Run a quick revenue‑multiple estimate.

- Perform an EBITDA‑multiple calculation.

- If you have growth potential, build a simple DCF model.

- Identify any owned assets, especially shared‑ownership homes, and calculate their NAV.

- Average the three methods, weighting them based on how reliable each set of data feels.

Comparison of Common Valuation Methods for a M Sales Business

| Method | Key Input | Typical Multiple Range | Resulting Value (Example) | Pros | Cons |

|---|---|---|---|---|---|

| Revenue Multiple | Annual Sales = $1,000,000 | 0.5× - 2.5× | $1.2million (1.2×) | Quick, easy, works when profits are hidden | Ignores profitability and cost structure |

| EBITDA Multiple | EBITDA = $150,000 | 4× - 8× | $900,000 (6×) | Focuses on cash‑generating ability | Requires clean EBITDA figure |

| Discounted Cash Flow | Projected cash flows, discount rate 10% | Variable (model‑based) | $950,000 - $1million | Captures growth and risk | Data‑intensive, assumptions drive result |

Common Pitfalls and How to Avoid Them

Over‑relying on a single method. Using only a revenue multiple can inflate value if margins are weak. Always triangulate with at least two approaches.

Ignoring seasonal cash‑flow swings. A retail shop might have high holiday sales that boost annual revenue but leave cash thin the rest of the year. Adjust cash‑flow projections accordingly.

Neglecting owner‑benefit adjustments. If the owner pays themselves a salary above market rates, the profit figure is overstated. Normalize earnings to market‑level compensation.

Forgetting tax implications. Taxes can erode cash flow dramatically. Use after‑tax cash flows in DCF models.

Next Steps - Turning Valuation Into Action

Once you have a ballpark figure, decide what you’ll do with it:

- Prepare a pitch deck if you’re looking for investors.

- Set a realistic asking price for a sale.

- Use the valuation to secure a business loan.

- Benchmark against competitors to spot operational improvements.

Remember, a valuation is a conversation starter, not a final verdict. Engage a professional appraiser or accountant for a formal report if you’re moving toward a transaction.

Frequently Asked Questions

What multiple should I use for a service‑based business with $1million sales?

Service firms typically trade between 0.8× and 1.5× revenue, depending on client concentration and repeat business. Start with 1× and adjust for profit margins.

How does owning shared‑ownership homes affect my business value?

Real estate adds a tangible asset layer. Calculate the net asset value of each property and add it to the income‑based valuation. This can raise the price by 10‑30% depending on market conditions.

Is a DCF model worth the effort for a small business?

If you have reliable cash‑flow forecasts and plan to grow, DCF gives the most nuanced view. For a stable, low‑growth shop, a revenue or EBITDA multiple may be sufficient.

What discount rate should I apply in a DCF analysis?

Small businesses often use a WACC between 10% and 15%, reflecting higher financing costs and market risk.

Can I sell my business for more than the calculated valuation?

Yes, if you have strategic buyers who value synergies, brand equity, or geographic reach higher than standard market multiples.